The Future of Insurance

New risks. New opportunities. Helping businesses stay in business, today and tomorrow.

Additional Content

Working at Argo

See how we're attracting a new generation of talent

Giving Back

Learn how we’re committed to our communities

Interviewee Bios

Learn more about our experts

Attracting Talent

Hear how insurance is attracting top tech talent

Blockchain

Learn about blockchain, and why it matters

Internet of Things

See how the Internet of Things is shaking up insurance

Digital Distribution

Hear about the future of digital distribution

Drones

Learn how drones are creating new risk for cities

Autonomous Vehicles

See how self-driving cars will change urban planning

Cyber Insurance

Learn why businesses are turning to cyber insurance

Impact of Natural Catastrophes

Read about the impact of natural catastrophes in 2017

Hurricanes and Flooding

Learn why hurricanes are getting more severe

Artificial Intelligence and Data

Learn how data and AI are transforming insurance

For the best experience,

Please rotate your device

Please widen your screen

Talent

Blockchain

Internet of Things

Digital Distribution

Drones

Autonomous Vehicles

Cyber Insurance

Natural Catastrophes

Hurricanes

Artificial Intelligence

Replay video

2017 was an important year for Argo. Despite significant, industry-wide catastrophe claims and underwriting challenges in the London market, our balance sheet held up well, and we finished the year in a better competitive position than we started.

We surpassed our 2017 gross written premium goal – up over 20% to $2.7 billion from $2.2 billion in 2016. Our net earned premium at $1.6 billion was 11.5% higher than the previous year. While our goal is to grow the bottom line first, over time it matters that we grow our business profile as well. 2017 was a good example of that.

Underwriting

After an extraordinary series of catastrophic events, we served our customers faithfully through expeditious claims handling. The resulting losses affected our bottom line, but they also remind us that we are fulfilling our mission: We’re here to help businesses stay in business. Our net exposure relative to our internal models was within reason for all the events we experienced, which equaled 7% of equity and 8% of net earned premium, well within the range of our peers. This equated to approximately $127 million in claims net for 2017 and a combined ratio of 107.2%, compared to 96.2% in 2016. Reflecting those losses and our experience in the London market, our net income was $50.3 million, compared to last year’s $146.7 million. It was, however, unfortunate that our acquisition of Ariel Re closed in the first quarter – meaning our net retentions for multiple reinsurance programs resulted in an additional impact on the bottom line. Going forward, we expect our net exposure to similar events to be close to 5 combined ratio points.

Investments

Our investment portfolio performed well again in 2017. We took deliberate steps to broaden the scope of our investment activity, and I am pleased to report investment income – even in a challenging environment – rose more than 21% to $140 million, compared to $115.1 million last year. This was aided by growing income from bonds and stocks, and a higher contribution from alternative investments. We continued building our assets, ending the year with cash and investments totaling almost $5 billion.

Capital management

During the year, we increased our dividends to shareholders by more than 25% to $1.08 per common share from $0.86 the year before, and we repurchased approximately 750,000 shares for $45.2 million. We believe the best measure of our long-term performance is based on book value per share. In 2017, our book value per share plus dividends grew by nearly 4%. For the last 15 years, including dividends paid, the compound annual growth in book value per share has averaged 9.4%.

U.S. tax reform

We are seeing early positive signs in the U.S. economy as a result of the new tax law, and we are optimistic it will create more growth among small to midsized businesses in America, which make up the core of the clients we serve. After an initial analysis of the law, we do not, however, expect a significant impact on our tax expense. In any period, the geography in which we earn profits determines our future effective tax rate. While we can’t know the outcome until the rules are written, we still anticipate an operating tax rate of approximately 20% or better going forward, keeping in mind it may vary each quarter depending on geography.

U.S. Operations

This was a good year for our U.S. business. Our excess and surplus casualty lines, surety, specialty programs and professional lines all benefited from targeted, tactical support, including digital systems improvement, team strengthening and marketing programs. All four businesses enjoyed important gains in both top-line and bottom-line growth. Casualty grew 26.8%, surety 27.7%, specialty programs 27.8% and professional lines 25.7% in top-line growth. In addition, our excess and surplus lines operation updated its technology yet again and can now respond to any submission within hours; in many instances, they can now respond within minutes. Rockwood grew 31.5% year over year by expanding its offerings well beyond its core clients’ mining-related exposures to include coverage for commercial automobile, pollution liability and surety. It’s telling that our increase in U.S. gross written premium was made within an overall market that was relatively static. Congratulations to Kevin Rehnberg and the heads of our individual businesses for their great success.

In 2017, U.S. gross written premiums were $1.5 billion, up $232 million or 18% over the same period last year. Underwriting income was $89.4 million, compared to $111.5 million in 2016. The combined ratio of 90.5% compares to 86.9% in the previous year. The primary differences were related to catastrophe activity and a number of non-recurring charges.

International Operations

As we would expect, given the risk portfolio, our International business was more heavily impacted by catastrophes during 2017. Despite these challenges, it remains an important part of our business for the future. In London, we concluded our ability to select risk can only go so far in the Lloyd’s subscription market – one of the toughest in the world – where we incurred large and more frequent losses over the year than expected. To reverse the trend, we added new leadership, reorganized our teams, strengthened our underwriting guidelines and raised our prices where needed. Because much of this work began in early 2017, our prospects look brighter for 2018.

In Bermuda, we acquired Ariel Re and integrated that company’s Lloyd’s syndicate, reinsurance operations and insurance operations into our own. We also welcomed Jorge Luis Cazar as our new head of Latin America and Matt Harris, our new head of Europe, Middle East and Asia, to lead our strategies for growth in those markets.

In 2017, gross written premiums were $1.2 billion for this segment, up $300.5 million or 33.9% over the same period last year. In 2017, we had an underwriting loss of $111.2 million, compared to underwriting income of $25.8 million in 2016. The combined ratio of 117.5% compares to 95.4% in the previous year.

“Today, we talk about such advances as drones, autonomous vehicles, augmented reality and artificial intelligence. These are not merely categories of risk that require expert underwriting. They are themselves engines of innovation that will create opportunity for insurers who are able to look ahead and who are willing to keep pace.”

The future of insurance

For more than a decade, we have been anticipating the transformation currently underway in our industry, predicting the unavoidable disruption of our value chain, service delivery and capital structure. Today, I want to provide a few thoughts on how we are thinking about the future. First, the steady stream of capital into insurance has produced overcapacity, which has in turn pushed margins down as investors compete to put their money to work. Second, the entry of all-digital players into the insurance business has posed a serious threat to legacy carriers, which are now struggling to become tech-savvy and customer-focused.

But will all-digital companies backed by fresh investor capital shake up our industry even further? We don’t think so. There is an advantage to understanding the rules, owning the data and building on a history of underwriting and risk management expertise. In our opinion, the judicious use of cutting-edge technology combined with insurance expertise represents the clear and, for established insurers, successful path to continued growth. By building digital expertise, often by forging creative partnerships with existing technology players, we can collaborate in ways that bring capital closer to the risk, reduce the complexity of our offerings and provide even greater value to our customers. But responding to shifting economic and consumer demands is not the only reason to change. We must also recognize and respond to the larger forces at play in the world and the risks they pose to our customers and to our own business as underwriters.

Last year, we continued our evolution. Under the guidance of Argo Digital, our talented team from inside and outside the insurance industry, we iteratively developed new software, invested in leading and emerging technologies and partnered with startups to devise technology that can overcome remaining bottlenecks in our business systems. To make underwriting faster, smarter and more accurate, we are now finding ways to leverage artificial intelligence, while processing vast amounts of new data from sources as varied as sensors, drones, government databases and social media.

We evolved our technology in 2017 to more efficiently connect with our distribution partners and their customers. For example, our digital Protector platform now serves 2,400 brokers and more than 50,000 active customers in Brazil. We launched a sensor-based technology that lets operators of restaurants, supermarkets and other retail businesses reduce the frequency and severity of customer and employee accidents. We built and launched a digital account-management environment where brokers and policyholders can find information they need quickly. We are partnering with a cybersecurity startup to give our customers the tools they need to prepare for and respond to cyberattacks.

Technology advancements in every domain will create new risks for people and businesses, of which cybercrime is a clear example. Cyber risks are unique in that they are both unlimited and perpetual. As an industry, we have little experience assessing the possible impact of new hacking technologies against multiple smaller entities. Imagine the losses following concurrent attacks against one million small businesses, the shutdown of every self-driving car, or perhaps just the bricking of every digital door lock. The payouts could be massive, and yet today’s premiums cannot truly reflect the scope of the risk, because we do not always know what that scope is.

As we look to the future of insurance, the risk posed by natural catastrophes will also evolve. Predictive climatology suggests that hurricanes, droughts, fires and floods will increase in magnitude. Melting ice fields at the North and South poles support forecasts of warmer weather and rising sea levels. Given the density of population and volume of business activity in coastal areas, revised assessments of the nature of catastrophic risk at or near sea level is imperative. As claims mount following these catastrophes, either pricing of insurance will have to rise or the scope of coverage contract. And while there is no direct correlation between sea temperature and the frequency of hurricanes, we now have ample evidence showing how much more quickly they can intensify – look no further than the storms of 2017.

Of teams and commitment

With some 400,000 industry professionals set to retire within the next five years, attracting talent is looming as a major issue for our industry. No amount of automation will overcome the need for talented and inventive professionals willing to take up insurance careers. Competition for their loyalty is strong. To attract them, we must prove that our industry is as dynamic and rewarding as we know it can be.

At Argo, we hold commitment to our employees and to each other as a central value, and one way we proved it again in 2017 was through the launch of Argo Academy, an online learning environment. In recognition of our focus on continuous learning, we were pleased to be named to Training magazine’s 2017 Training Top 125.

Also core to Argo’s culture is our employees’ deep commitment to the communities in which they live and work. In 2017, hundreds of Argo employees were involved in projects around the world. After Hurricane Harvey smashed the Texas coast in late August, thousands of homes and businesses were flooded. Argo employees moved into action. Making numerous trips between our U.S. headquarters in San Antonio and the Houston and Corpus Christi areas, they delivered much-needed supplies. They also spearheaded our corporate support of nonprofit organizations delivering relief, including the American Red Cross, the Insurance Industry Charitable Foundation and several local organizations.

The speed and variety of emerging risks is growing. Yet the factors I’ve mentioned – capital, climate, new risk and talent – are the home turf of specialty insurance at which Argo excels. Specialty insurance lives at the crossroads of new ideas and new threats. We are confident specialty underwriters will continue growing in importance as a critical support for new enterprises, enabling entrepreneurs to mitigate the considerable risks associated with early adoption of new technologies. Today, we talk about such advances as drones, autonomous vehicles, augmented reality and artificial intelligence. These are not merely categories of risk that require expert underwriting. They are themselves engines of innovation that will create opportunity for insurers who are able to look ahead and who are willing to keep pace. We will continue to be one of them.

Mark E. Watson III

Chief Executive Officer

For the second year in a row, Forbes magazine named Argo Group to its list of America’s 50 Most Trustworthy Financial Companies.

In January, we launched Argo Risk Tech, a state-of-the-art web-based inspection platform that helps minimize workplace risk.

Our acquisition of Ariel Re earned Insurance Insider Honours for M&A Transaction of the Year.

Argo Seguros was named Brazil Insurer of the Year in the annual Reactions magazine Latin America Awards.

Bryan Mortimer, an Argo Surety mining engineer, was granted a U.S. patent for co-inventing a ventilation system to repurpose methane exhaust in mines as an energy source for surface refineries.

Reigning World Touring Car champion José María “Pechito” López joined Argo-sponsored Formula E team Dragon Racing as a driver in the 2017-2018 season.

Argo Group was honored with the CIR Risk Management Operational Risk Initiative of the Year award for the risk assessment we conducted during our deal to acquire Ariel Re.

(Excellent)

A.M. Best rating for 13 years in a row

Nautical miles the Argo-sponsored team Vestas 11th Hour Racing will sail across four oceans during the 2017-2018 Volvo Ocean Race

Square feet gained in Argo’s new LEED-certified office in New York City’s Meatpacking District

Average percentage of employees who refer others to work at Argo every year

Number of employees recognized for outstanding achievements by insurance industry publications

Gross Written Premiums

in billions

Argo Group gross written premiums grew to $2.70 billion in 2017, a 25% increase compared with $2.16 billion in 2016.

U.S.

$1.51

International

$1.19

Total Assets in billions

21.5% increase in 2017

Combined Ratio

11.4% increase in 2017

Book Value Per Share

4.6% increase in 2017

Despite the challenges posed by intense weather events, Argo’s U.S. Operations achieved a fifth consecutive year of profitability in 2017. Our claims teams worked around the clock, responding quickly and fairly to claims arising from extensive damage caused by natural disasters. While hurricane, fire and flood activity dampened our reported bottom-line results, our businesses stayed focused and performed exceptionally.

Targeted investment in four high-potential areas

Last year, we identified four business lines with high growth potential and gave them additional resources to accelerate their growth. We made sure they had the right people in the right roles making wise decisions. We teamed business leaders with process-optimization experts and digital-systems developers to re-engineer the way they do their work. And we harnessed the strength of the Argo brand, demonstrating to customers how Argo’s specialty underwriting expertise and financial stability can help them grow their own businesses.

Excess and Surplus

Within our excess and surplus lines (E&S), we underwrite primary and excess casualty, property and professional liability coverage for hard-to-place risks. To propel our casualty business last year, we placed top talent in key positions, overhauled most of our internal processes and made it easy for our producers to work with us. Notably, we found ways to further accelerate our submissions process. Able to respond to any submission in fewer than five hours, Argo now stands in a class of its own.

Argo Surety

Surety is a complicated and competitive business, but we have a keenly competitive appetite and a broad portfolio of offerings. In 2017, we strengthened our surety contract team with a number of seasoned industry professionals eager to join our growing enterprise. That larger team is now using its deep underwriting expertise to build solid, enduring and profitable relationships within an expanding base of clients.

Argo Pro

Argo Pro is our mid-market professional lines platform. In a year of strong performance, we made improvements across a broad spectrum of activity. We rebuilt all our forms and contracts from scratch, making it easier for our producers and their customers to work with us. At the end of the year, we helped launch Coalition, a unique combination of digital tools and insurance coverage designed to help organizations address the threat of cyberattack.

U.S. Specialty Programs

A year of strong growth in this business came from both simplification and expansion. To simplify, we sold renewal rights to a number of our agency programs, choosing to concentrate wholly on our services as a risk-bearing carrier. To expand, we worked with our partners and producers to pursue opportunities in new areas. We successfully implemented three mature, profitable books of business that substantially increased our revenue, providing scale for steady, sustainable future growth.

Gross Written Premiums in billions

18% increase in 2017

Targeted support leads to U.S. growth

In 2017, these four business units were growth priority areas. The year-over-year results are notable.

2017 year-over-year growth in gross written premium

2017 was a pivotal year for Argo’s International Operations. Building on our solid foundations in Bermuda and London, we took decisive action to expand our global footprint. First, we put top-performing industry professionals in critical leadership roles. Next, we made acquisitions that brought us new teams, platforms and customers around the world. Finally, we took deliberate steps to deepen our presence in Europe, Latin America and Asia.

Bermuda

Our acquisition of Ariel Re in February brought us new tools and talent, and gave us the scale we sought in both our reinsurance business and our London operations. With Argo Re and Ariel Re operating under a single banner, we now offer our reinsurance customers alternative risk-transfer solutions, leveraging our insights supported by data analytics and modeling capabilities. We restructured our insurance operations in Bermuda to better serve the evolving needs of our clients. We also strengthened our property business by adding the team of property underwriters that came from the Ariel Re acquisition to our existing team of Argo property experts. Late in the year, we unified our international open-market property businesses to allow our London, Bermuda and U.S. teams to participate on joint accounts and better deploy our growing capacity.

United Kingdom and Europe

In London, we organized our Lloyd’s syndicates 1200 and 1910 efficiently under a single Argo Managing Agency. Under the watchful eye of a newly appointed international chief underwriting officer, we worked to exercise more rigorous underwriting discipline, refusing to chase top-line growth in one of the industry’s most challenging markets. We appointed a new head of Europe, who now leads our effort to find the right geographical mix as we grow across the continent. We added a team of underwriters to capitalize on new opportunities in Germany, Austria and Switzerland, and we successfully introduced our specialty product capabilities into southern Europe.

Latin America

With a new head of Latin America onboard, we opened an office in Miami to allow us to explore opportunities in the fast-growing facultative market and to serve as a launching pad to explore profitable growth opportunities, including a variety of new markets in both Central and South America. Our operation in Brazil once again produced good results. Despite the barrage of economic and political challenges that perplex that country, we grew our core business in Brazil by 21 percent; through our digital Protector platform, we now serve over 50,000 active customers through a network of more than 2,400 producers. Our ability to identify untapped market niches, create new ways of doing business and provide superior coverage earned us a nod from Reactions Latin America Awards as Brazil’s Insurer of the Year.

Asia

With offices in Shanghai and Singapore, we were able to drive business successfully in two highly complex markets. Our focus in Asia, as always, is to find unique opportunities where our long experience as specialty underwriters allows us to compete, even against much larger carriers. Last year, we continued that approach by opening a center in Hong Kong, where our expertise in sustainable energy has attracted the interest of businesses ready to launch infrastructure projects related to clean, renewable power.

Gross Written Premiums in billions

33.7% increase in 2017

An expanding global presence

As a leading global specialty underwriter, we do business around the world.

Barcelona

Bermuda

Brussels

Dubai

London

Malta

Milan

Paris

Rio de Janeiro

Rome

São Paulo

Singapore

United States

Zurich

As we grow, we’re committed to securing the future for our employees, just as we are for our clients, shareholders and communities.

We start by hiring the best people. “We’re pushing boundaries to attract the best and brightest,” says David Harris, head of group performance. “This is something the insurance industry hasn’t always done.”

One reason insurance is attracting a new generation of digital talent? “This is one of the original data businesses,” says Andy Breen, senior vice president of digital. “People see that they have the opportunity to actually evolve the business from the inside by applying artificial intelligence and machine learning.”

Success depends on keeping our employees engaged and challenged, and providing opportunities for growth.

We have an entire team dedicated to training and development. And we give employees opportunities that range from an annual leadership conference at Harvard Business School to Argo Academy, a companywide platform for continuing education that offers 250,000 tailored courses. We also have partnerships with organizations such as Bell Leadership Institute and Stanford University.

“When we invest in our employees,” says Harris, “they feel a pride in and ownership of the organization.”

Download the PDF version of the 2017 Annual Review

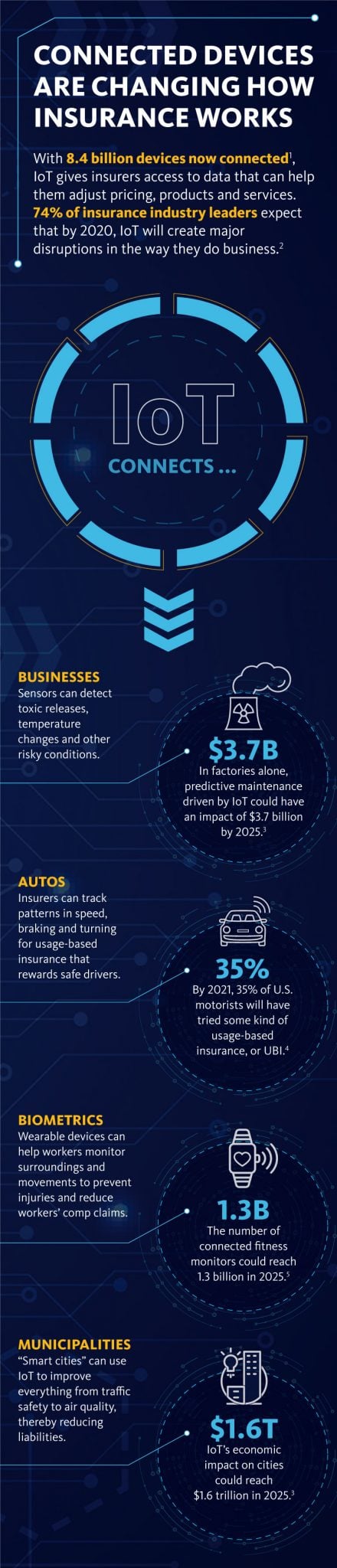

Connected Devices are Changing How Insurance Works

With 8.4 billion devices now connected1, IoT gives insurers access to data that can help them adjust pricing, products and services. 74% of insurance industry leaders expect that by 2020, IoT will create major disruptions in the way they do business.2

- https://www.gartner.com/newsroom/id/3598917

- http://www.businessinsider.com/internet-of-things-insurance-home-life-auto-trends-2016-10

- https://www.mckinsey.com/~/media/McKinsey/Business%20Functions/McKinsey%20Digital/Our%20Insights/The%20Internet%20of%20Things%20The%20value%20of%20digitizing%20the%20physical%20world/The-Internet-of-things-Mapping-the-value-beyond-the-hype.ashx

- http://www.businessinsider.com/internet-of-things-insurance-home-life-auto-trends-2016-10

- http://www.healthcareitnews.com/news/iot-potential-understated

Insurance Industry Faces Climate Change Challenges

As the global climate continues to warm, the intensity of hurricanes and related storms as well as wildfires is projected to increase.

- https://www.nhc.noaa.gov/data/tcr/AL092017_Harvey.pdf

- https://www.reuters.com/article/us-storm-harvey-corelogic/harvey-residential-insured-and-uninsured-flood-loss-25-37-billion-corelogic-idUSKCN1BC3Z1

- https://www.iii.org/fact-statistic/facts-statistics-wildfires

- http://www.businessinsurance.com/article/20171117/NEWS06/912317338/Northern-California-wildfires-to-be-costliest-in-US-history-Fitch-Ratings

- https://www.munichre.com/en/media-relations/publications/press-releases/2018/2018-01-04-press-release/index.html

- https://www.nytimes.com/2017/08/29/world/asia/floods-south-asia-india-bangladesh-nepal-houston.html?_r=0

- https://www.epa.gov/climate-indicators/climate-change-indicators-sea-surface-temperature

- https://www.ucsusa.org/global-warming/global-warming-impacts/when-rising-seas-hit-home-chronic-inundation-from-sea-level-rise#.Wm8z-bQ-eCQ